Quarterly Outlook

Q3 Investor Outlook: Beyond American shores – why diversification is your strongest ally

Jacob Falkencrone

Global Head of Investment Strategy

Key points:

------------------------------------------------------------------

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

Disclaimer: Past performance does not indicate future performance.

In the news:

Macro:

Macro events: NZ May Business, NZ Manufacturing PMI, NZ May Food Prices, Japan April F Industrial Production, BOJ’s Kazuo Ueda speaks, Hong Kong 1Q Industrial Production & PPI, BOJ Rate Decision. China May New Lending, Money Supply

Earnings: CarMax, FactSet

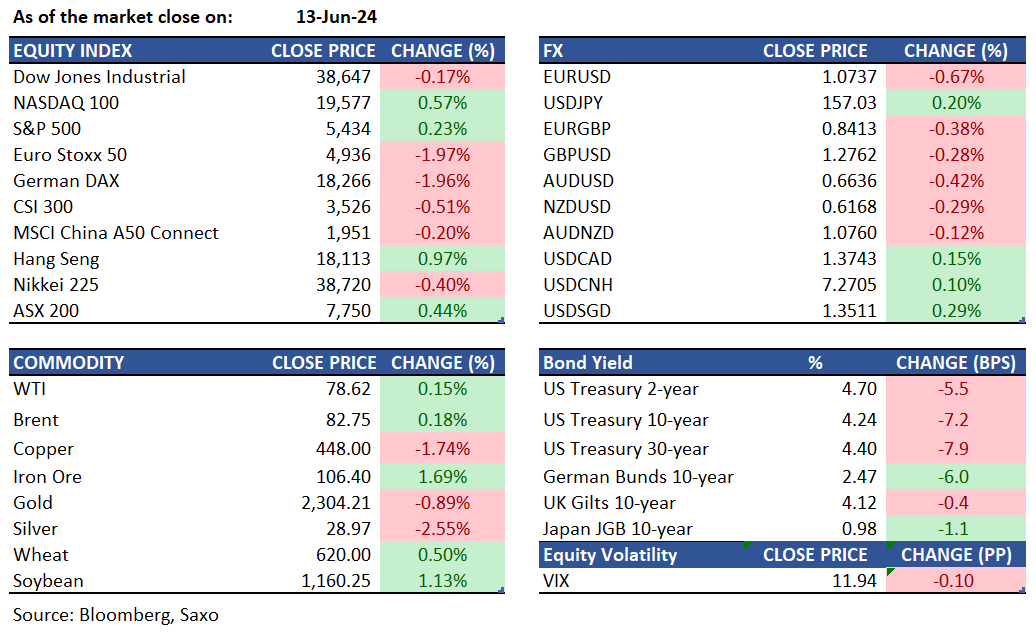

Equities: Equity markets showed little change on Thursday, with the S&P 500 and Nasdaq slightly up and the Dow dropping over 60 points. The S&P 500 reached a record high above 5,400 on Wednesday due to positive sentiments to the latest consumer price inflation report. Technology, real estate, consumer staples, and utilities performed well, while small-caps and industrials lagged. Chip stocks in general helped to lead the markets higher. Markets in general are still holding/ trading near record highs despite the US central bank dialing back rate cut expectations for this year.

Fixed income: Money-market fund assets reached a new high, with approximately $28 billion entering US money-market funds in the week ending on June 12. Total assets increased from $6.09 trillion to $6.12 trillion, surpassing the previous record set in April. Meanwhile, 10-year Treasury yields dropped by seven basis points to 4.24%. The European Union's bonds were negatively affected as expectations of their imminent inclusion in important sovereign benchmarks suffered a setback, leading to increased political uncertainty in France. In Japan, bond futures advanced ahead of the Bank of Japan's upcoming policy announcement, with the benchmark yield decreasing by 2 basis points to 0.965% on Thursday. Economists anticipate the BOJ to maintain its benchmark interest rate and reduce the pace of bond purchases from around ¥6 trillion per month. Additionally, the 10-year yield in New Zealand dropped by 4 basis points to 4.63%, while the yield on Australia's 10-year debt fell by 5 basis points to 4.14%.

Commodities: Oil price surged as indications of easing U.S. inflation, potentially leading to a Federal Reserve interest rate cut. However, the market's gains were tempered by a surprising 3.73 million barrel increase in US crude stockpiles, as well as larger-than-expected increases in US gasoline and distillate stocks. The ongoing situation in Gaza, with ceasefire negotiations and Red Sea shipping attacks, is also being closely monitored. Silver prices fell to a one-month low of $29 per ounce due to a more hawkish stance from the Federal Reserve, despite weaker inflation data. The impact was offset by recent dovish actions from major central banks. The US imposed 50% tariffs on Chinese imports of solar cells, impacting the silver industry, but strong demand in the Chinese market limited further declines in silver prices.

FX: The dollar, along with other safe-haven currencies, strengthened as market sentiment turned cautious following a relatively hawkish Federal Reserve dot plot and concerns about the French election weighing on the euro. The Bloomberg Dollar Spot Index rose by 0.1% after initially dropping to the day's low following PPI data. EUR/USD declined by 0.7% to 1.0739, approaching the weekly low of 1.0720 due to cross-related sales and downside option purchases after significant expiries at 1.0770-80 expired. USD/JPY increased by 0.1% to 156.93, with attention focused on the Bank of Japan's policy decision on Friday. Overnight volatility surged to approximately 15%, the highest level since early May but still below recent meeting dates. GBP/USD decreased by 0.3% to 1.2760. USD/CAD was up by 0.2% at 1.3746, as Deputy Governor Sharon Kozicki defended the use of quantitative easing and extraordinary forward guidance during the pandemic. AUD/USD fell by 0.4% to 0.6638 due to weakness in metal prices and the offshore yuan.

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration.

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy