Quarterly Outlook

Equity outlook: The high cost of global fragmentation for US portfolios

Charu Chanana

Chief Investment Strategist

Summary: A sustainable finance ecosystem requires a huge reallocation of capital.

In a world mired by enduring challenges there has undoubtedly been significant progress so far this century. Globalisation, free markets and technological advances have generated unprecedented wealth and opportunity for some, lifting millions out of extreme poverty and engendering welfare improvements seen across many important indicators such as child mortality and access to basic education.

However, public debate is plagued with populist agendas, crises in economic activities, climate anxiety and rising inequality, which are supplanting free-market capitalism and expanding democracy as key themes. As the third decade of the millennium begins we are on the cusp of an inflection point where the economic and environmental losses and social impact of maintaining the status quo are unsustainable. As policymakers, prudential supervisors, investors and the corporate community alike recognise that their future is inextricably linked to a sustainable economic operating model, growth at any cost will no longer be viable. This will shape the future policy agenda and reallocation of global capital with increasing immediacy.

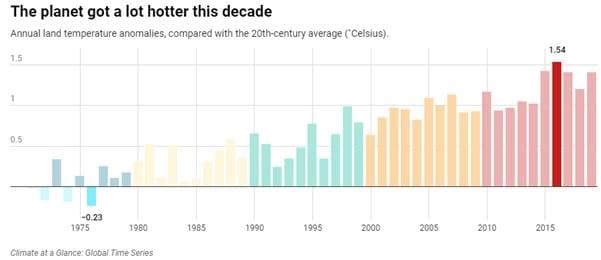

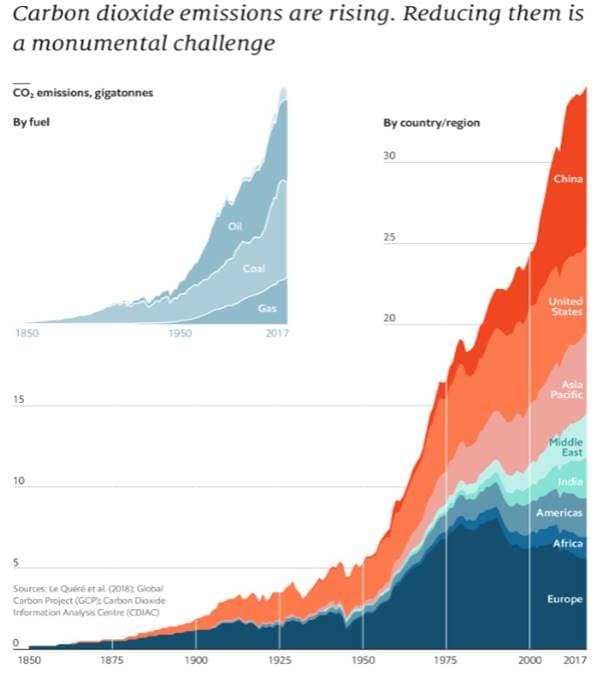

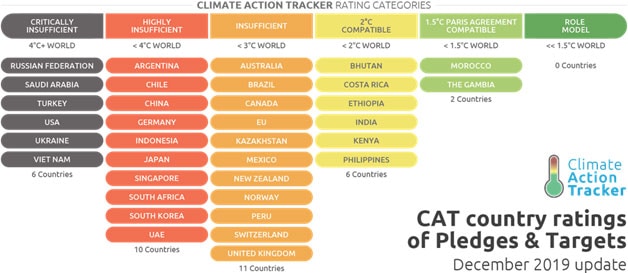

Honing in on the key focus of this report, the climate, it is our view that the prior decade, which has been the hottest in history, marked peak indifference on climate change. Despite years of debate, global greenhouse gas emissions are reaching record levels and show no sign of reversing.

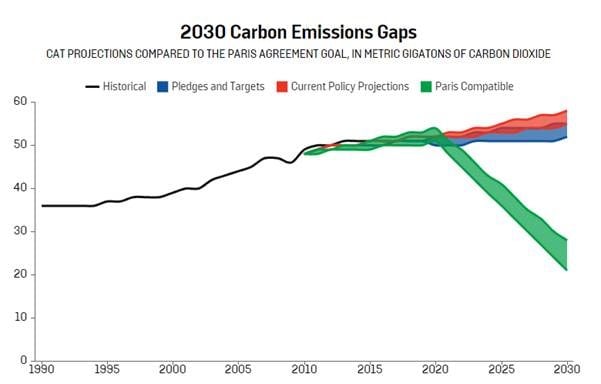

Source: Climate Action Tracker

Rising temperatures have not only melted Arctic ice far quicker than predicted and bleached coral reefs, but also exacerbated the intensity and frequency of deadly droughts, hurricanes, heat waves, and wildfires.

The devastating loss of life and nature demonstrates the significant cost of inaction on climate change. It provides a stark reminder that we are teetering on the edge of a tipping point, where the changes to our planet far outpace any nation’s ability to adapt to them.

Although there are wide margins of error in forecasting the potential impact and many uncertainties remain, the greatest challenge of the 21st century could well be the decarbonising overhaul of the global economy.

Global warming has seen average air temperatures rise by more than 1°C since records began in 1850, and each of the last four decades has been warmer than the previous one. Sea levels globally have risen 20cm since 1880 at a rapidly accelerating rate, increasing the risk of flooding. Weather patterns, meanwhile, have been altered — hindering food security.

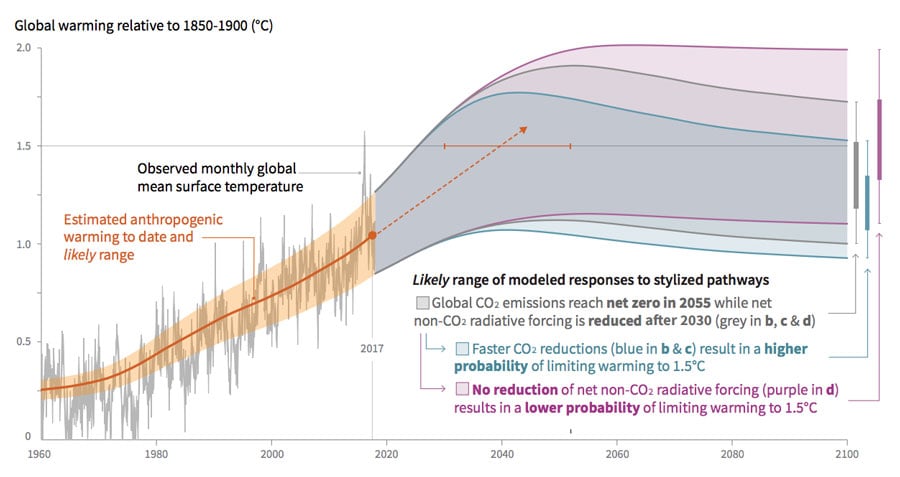

The failure to halt emissions growth over the last 10 years could limit the world’s ability to shift to a pathway consistent with 1.5°C or even 2°C of global warming, the upper end of the Paris Agreement's goal (Intergovernmental Panel on Climate Change). According to Climate Action tracker, as of December 2019 under current pledges, the world will warm by 2.8°C by the end of the century — close to twice the limit agreed in Paris. In terms of real policy action, see temperatures could rise by 4°C .

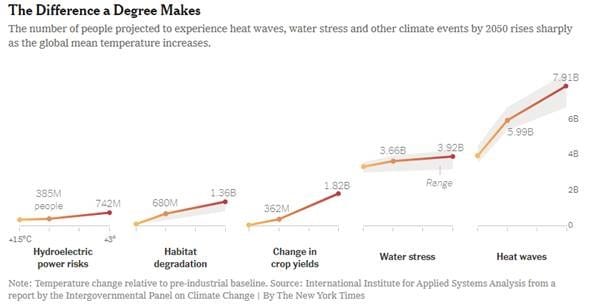

Accelerated warming has huge implications for our planet’s oceans, land and atmosphere. For example, scientists at Climate Central estimate that 275 million homes could be submerged at 3°C global warming, with Asian cities most affected. Many land and seaborne species would face mass extinctions.

Aside from the devastating loss of biodiversity in the natural world, this threatens vital marine and land ecosystems upon which billions of people rely for food and employment. According to the scientific report released by WWF warming of 2°C would be untenable for 25% of species in Madagascar, which would cause their extinction by the 2080s.

Beyond 3°C, scientists estimate the frequency of high temperature events will at least double compared to present day and extreme precipitation will become not only more intense but also more frequent, making disaster induced displacement a growing risk factor.

Those already facing poverty will be hardest hit, thus exacerbating inequality.

27 of the world's 28 poorest countries are in sub-Saharan Africa where a combination of dependence on agriculture, environmental deterioration, and population growth are deadly. Here, the primary cause of migration is often climate induced. Weak institutions are unable to adapt to climate changes and when people have nothing to eat, they are willing to pick up a gun to survive.

The cascading effects resulting from constraints like food and water security concerns or homes and livelihoods lost to natural disasters will result in serious ramifications that are too great to ignore. The world has agreed immediate action is necessary, and as the costs of apathy mount implementation is more crucial than ever.

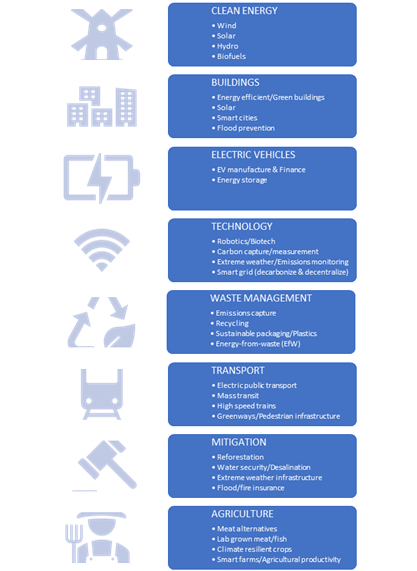

Climate action could be one of the most transformative and disruptive challenges faced by the global economy. For investors in global capital markets, aside from the obvious negative implications to any industry reliant on fossil fuels, the impact will be far reaching affecting industries from finance to REITs and transportation. The green transformation will also drive many positive advances as the need for adaptation spurs the adoption of policy solutions aimed at funding clean energy projects, water security, sustainable infrastructure developments and green technological innovations such as emissions capture and energy storage breakthroughs. These new climate industries not only provide jobs and economic gains but also generate a positive impact by providing cleaner air, preserving delicate ecosystems and improving human health. The climate crisis is defining a future generation, and as the cohort of millennial and Gen-Z investors grows financial performance will no longer be the only investment goal, increasing demand for positive impact investments that align with broader sustainable objectives.

Creating a sustainable finance ecosystem requires a huge reallocation of capital. Investors and corporates who do not gear their portfolios towards more sustainable business models risk facing large losses in the coming decades: regulatory changes could leave many current operating models unviable. Over a third of global capital already has some form of ESG mandate, putting many companies and countries on the wrong side of that mandate on the backfoot. If companies fail to adjust, they will cease to exist.

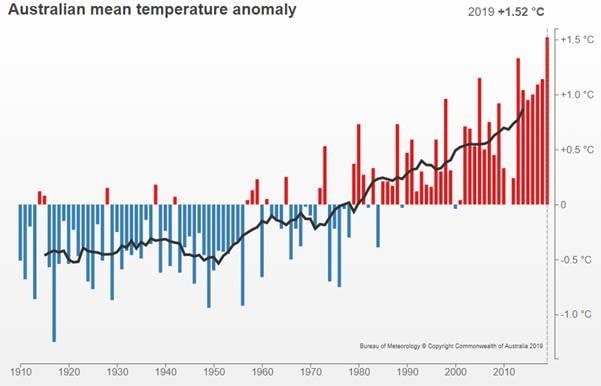

Australia, the world’s driest inhabited continent and home to fragile ecosystems like the Great Barrier Reef, is ground zero for climate change and particularly vulnerable as our planets temperature rises. Australia's climate alone has heated by more than 1°C since 1910. In fact, 2019 was the hottest and driest year on records dating back to 1910, according to the Bureau of Meteorology. From extreme heatwaves to heavy rain, severe droughts to deadly wildfires, a decade of unprecedented warming has seen the frequency and cost these extreme weather events increase.

Giving the rest of a world a glimpse at what the climate crisis may bring in the coming decade, these record-breaking temperatures and dry spells have fuelled an unprecedented bushfire crisis that has so far laid bare over 10million hectares of land. Destroying homes and livelihoods, and wiping out an estimated 1.25 billion native animals, “hastening extinction” for some species according to Professor Chris Dickman, University of Sydney. A tipping point that incites remedial action to minimise climate related risks, as prevention becomes less costly than the cure.

The ongoing bushfire crisis will present a headwind for the economy in the near term, which is already experiencing a period of soft economic growth. The full impact is hard to gauge and will be moving target as continued hot dry weather presents the risk of the fires intensifying further, but will no doubt cost the economy billions of dollars, with the bulk of the damage felt in Q1 2020. The damaging disruption to tourism, regional trade, construction activity, agricultural productivity and retail, against the backdrop of an already cautious consumer, will not only hit those areas most affected, but also major East Coast cities engulfed by thick smoke. Tourism is Australia’s 4th largest export and could suffer a lasting blow as devastating images of burning animals and cities shrouded in smoke, leaving the air quality worse than Delhi, Mumbai and Beijing, flood international newsfeeds.

All this comes at a time when the underlying economy is already weak. Consumer’s confidence in the economic outlook, which was already supressed, has been mired further by the ongoing crisis hitting lows not seen since 1994 on some measures. The outlook for consumption is not only pressured by poor confidence inhibiting the consumers propensity to spend, but also by ongoing concerns surrounding job security, stagnant wage growth and excessive household debt levels.

Several quarters of below trend economic growth, along with weak consumer spending , poor business conditions and a private sector in recession presents a deteriorating outlook for the labour market and employment growth. This whilst unemployment remains well above the RBA’s full employment estimate, inhibiting wage and inflationary pressures from materialising.

Before bushfires presented a headwind for confidence and economic activity, we expected the RBA to cut the cash rate again in February and once more later in 2020. Whilst not a direct factor, the present disruption only reinforces our view and adds to the board’s impetus to deliver another 25bp cut in February, particularly whilst the government leave the heavy lifting to the central bank. This will see both the AUD and Aussie bond yields shackled by the domestic outlook, with reflationary bounces short lived and strength sold into. We believe it is too early to maintain an outright bullish bias on AUD, despite an ongoing recovery in risk assets and receding geopolitical risks.

A UN report finds that to even come close to the goal of limiting global warming to 1.5°C over the next decade, nations must halve emissions by 2030. According to Climate Action Tracker, after removing highly unpredictable LULUCF changes to focus solely on energy and industry emissions Australia’s Paris target translates to a 14-16% decrease from 2005 levels by 2030. But under current policies, Australian emissions are headed for an increase of 8% above 2005 levels by 2030. Climate policy is actually worsening as coal fired power generation is greenlighted with little regard for the coal phase out obligations of the Paris Agreement in OECD countries by 2030. And that is before accounting for the fossil fuel intense exports that Australia ships elsewhere.

But we are fast approaching an inflection point, as climate change starts to constrain economic growth where the cost of inaction outweighs the cost of action. In Australia, the current governments denial of the world’s leading advice on climate change puts them on a collision course with both society and investors. The present crisis is defining a new generation of Australians, research from The Australia Institute has found that 2/3s of Australians believe the country is facing a climate emergency and that the Government should mobilise all of society to tackle the issue, like they did during the World Wars.

If the 2020s are the decade of cleaner, greener change then investors and policymakers must allocate toward sustainable business models or face large losses. Climate change presents challenges that are complex and unprecedented, but mitigation efforts will require systemic changes, providing multiple opportunities for investors.

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Head of Fixed Income Strategy