Quarterly Outlook

Q1 Outlook for Traders: Five Big Questions and Three Grey Swans.

John J. Hardy

Global Head of Macro Strategy

Strap yourself in for key market questions that must be answered in 2026.

Summary: Covered calls and cash-secured puts can help long-term investors make portfolio decisions more deliberate by linking option trades to shares they already own or cash they are willing to deploy. The key is not chasing premium, but understanding the obligation: selling shares at a chosen price or buying them at a chosen level.

Two option strategies for investors who want to use shares or cash more deliberately.

Many long-term investors hear the word “options” and immediately think about speculation or high-risk trading. That reputation exists for a reason, but it is only part of the picture. Some option strategies are designed around shares or cash an investor already has.

Two of the most widely used examples are the covered call and the cash-secured put. Both strategies involve selling an option and receiving premium upfront. In return, the investor accepts an obligation. With a covered call, that obligation is to sell shares at a predetermined price. With a cash-secured put, it is to buy shares at a predetermined price.

That distinction matters because the right strategy often depends less on market forecasts and more on the investor’s starting point. Do you already own shares that you would be willing to sell at a higher price? Or do you have cash available and would be happy to buy shares at a lower price?

For many buy-and-hold investors, that is the real decision.

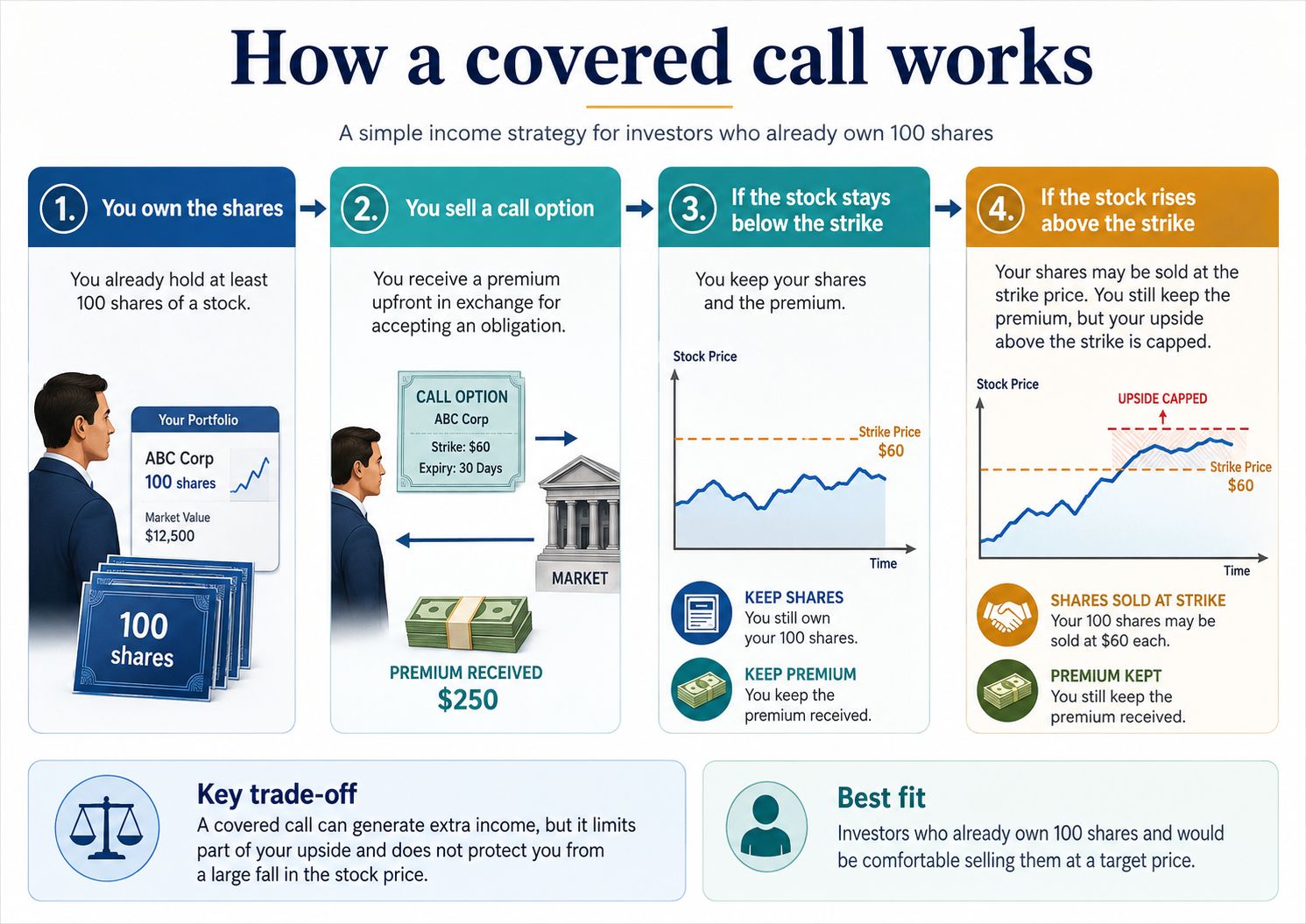

A covered call starts with an existing share position. The investor owns at least 100 shares and sells a call option against those shares.

By selling the option, the investor receives premium income upfront. In exchange, they agree to sell the shares at the strike price if the option buyer decides to exercise the contract.

In simple terms, a covered call allows an investor to generate additional income from shares they already hold, while accepting that the upside above the strike price is limited.

A covered call can generate income from shares you already own, but it limits potential gains above the strike price. Source: Saxo

Imagine an investor owns 100 shares of a company trading at EUR 50. The investor sells one call option with a strike price of EUR 55, an expiry one month away, and a premium of EUR 1.50 per share. Because one listed equity option typically represents 100 shares, the investor receives EUR 150 in premium before transaction costs.

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it’s crucial to make informed decisions.

From here, three broad outcomes are possible:

The premium provides a small buffer against losses, but it does not eliminate the downside risk of owning the shares. A covered call is still primarily an equity position. The option income can slightly improve returns or reduce the impact of a modest decline, but it does not fully protect the portfolio during a large sell-off.

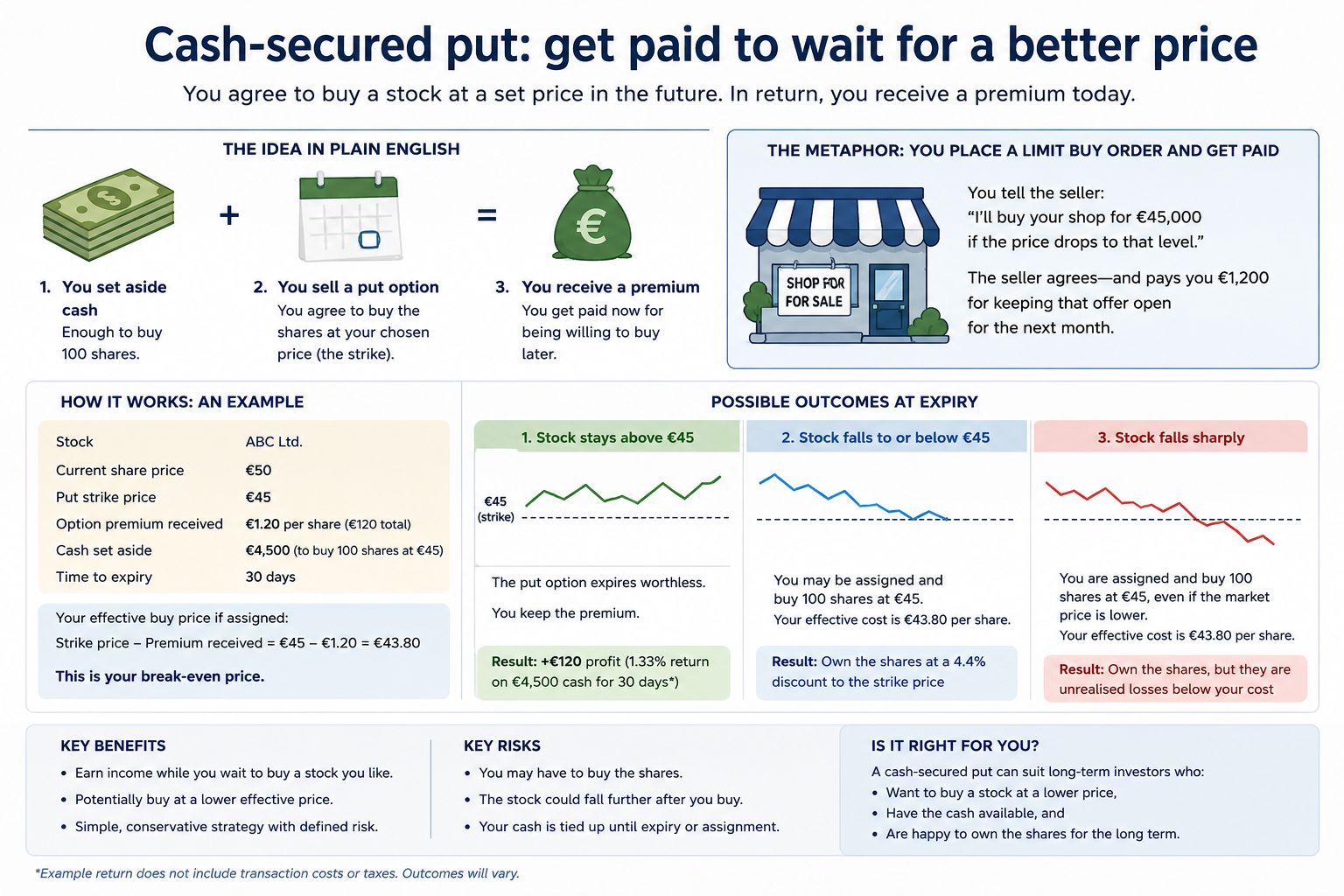

A cash-secured put works differently. Instead of starting with shares, the investor starts with cash.

The investor sells a put option and sets aside enough cash to buy 100 shares if assigned. In return for accepting that obligation, they receive premium upfront.

In practical terms, a cash-secured put can be viewed as a disciplined way of expressing willingness to buy a stock at a lower price.

A cash-secured put can generate income while waiting to buy shares, but the investor must be willing to buy if the stock falls below the strike price. Source: Saxo

Using the same stock at EUR 50, the investor sells a put option with a strike price of EUR 45, an expiry one month away, and a premium of EUR 1.20 per share. The investor receives EUR 120 in premium before transaction costs and sets aside EUR 4,500 in cash in case the shares must be purchased.

From here, three broad outcomes are possible:

The premium lowers the effective purchase price slightly, but it does not remove the risk of buying a declining stock. For that reason, cash-secured puts are generally most appropriate for stocks the investor would genuinely be comfortable owning for the long term.

Although the two strategies are often compared, they usually solve different problems. A covered call is typically used by investors who already own shares and would be comfortable selling them at a higher price. A cash-secured put is typically used by investors who have available cash and would be comfortable buying shares at a lower price.

Seen this way, the strategies are less about predicting markets and more about formalising decisions many long-term investors already make. A covered call says: “I would be willing to sell my shares at this level.” A cash-secured put says: “I would be willing to buy the shares at this level.”

One reason these strategies are often introduced to newer option investors is that they are linked to familiar portfolio decisions. The covered call is connected to an existing shareholding. The cash-secured put is connected to a potential future purchase.

Neither strategy relies on leverage in the way some more speculative option structures do. In both cases, the investor either owns the shares already or holds enough cash to meet the obligation.

That does not make the strategies risk-free. Both involve selling options, which means accepting obligations in exchange for premium. The premium is not free money. It is compensation for accepting a future commitment.

That distinction becomes especially important during volatile markets. A covered call investor can still face losses if the stock falls sharply. A cash-secured put investor can still be required to buy shares during a difficult market environment. As a result, many experienced investors focus less on the premium itself and more on whether they would genuinely be comfortable with the obligation attached to the trade.

Long-term investors often discover that the biggest risks in these strategies are behavioural rather than technical.

With covered calls, some investors become frustrated if the stock rallies strongly and the shares are called away. The premium income can feel attractive at the start, but the strategy can underperform a simple shareholding during sharp upward moves.

With cash-secured puts, investors sometimes focus too heavily on the premium and not enough on the stock itself. A high premium can occasionally reflect elevated market risk rather than a particularly attractive opportunity.

That is why many experienced investors begin with a stock they already understand and would be comfortable owning without the option premium.

A covered call can be viewed as setting a target sale price for shares you already own.

A cash-secured put can be viewed as setting a target purchase price for shares you would like to own.

In both cases, the option premium is the compensation for making that commitment. For investors who already think in terms of target buying and selling levels, that framework can make options feel less abstract and more connected to decisions they already make in traditional investing.

Covered calls and cash-secured puts are often presented as beginner-friendly option strategies, but they still require planning and discipline.

The key question is not whether the premium looks attractive. The key question is whether the investor would genuinely be comfortable with the obligation that comes with the trade.

A covered call may fit an investor who already owns shares and would be comfortable selling them at a predefined price. A cash-secured put may fit an investor who has available cash and would be comfortable buying shares at a lower level.

For long-term investors, that is often the most useful way to approach both strategies.

| Related articles/content |

|---|

| From shareholder to options user | 26 May 2026 Alphabet after earnings - how a covered call can help investors manage a strong rally | 30 Apr 2026 Tesla shares after earnings could a covered call make sense | 27 Apr 2026 A structured way to buy IWDA at a lower price using options | 20 Mar 2026 How to improve the yield on a long-term IWDA holdings | 12 Mar 2026 How to use a collar to protect stock gains - a Tesla case study | 20 Feb 2026 Palantir after earnings - using options to define a potential entry price | 4 Feb 2026 Golds pullback - thinking beyond buy or sell | 3 Feb 2026 Why options got so popular in recent years | 28 Jan 2026 Netflix earnings - using a cash-secured put to set a lower entry price | 16 Jan 2026 |

| More from the author |

|---|

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Global Head of Investment Strategy