Macro: It’s all about elections and keeping status quo

Markets are driven by election optimism, overshadowing growing debt and liquidity concerns. The 2024 elections loom large, but economic fundamentals and debt issues warrant cautious investment.

Head of Commodity Strategy

Crude oil has pared back some of the overnight gains that was attributed to another failed missile strike on Saudi Arabia from Houthi forces within Yemen. The price of both WTI and Brent crude oil almost reached the January peaks with a rejection leaving many fresh longs at risk. A break, however, could see WTI target a minimum of $70/barrel.

Source: Saxo Bank

Last week’s surge was driven by a combination of the technical breakout of the triangle formation and renewed worries that Iranian production and exports could be negatively impacted should Trump decides to reinstate sanctions after May 12.

Against these developments we saw global trade tensions tear into global stocks. This helped create a major and potentially unsustainable dislocation between the two. Additional stock weakness driven by the risk of an escalating trade war could reduce global growth and ultimately this would translate into a lowering of global demand growth for oil.

Iran and trade tension focus helped trigger a major divergence between global stocks and oil prices last week.

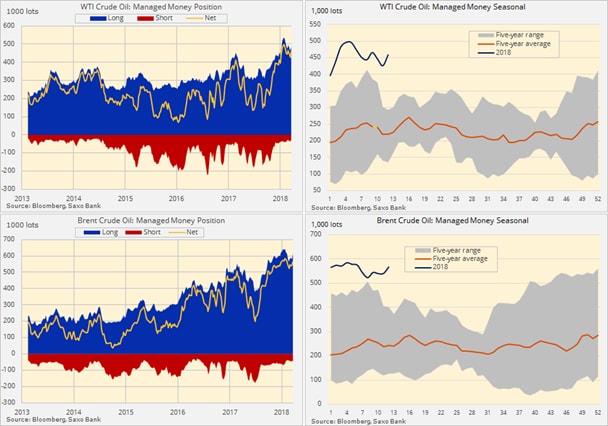

For now the risk of lower supply combined with robust demand and a high level of Opec compliance to the agreed production cut deal have triggered another round of speculative buying with hedge funds increasing the combined net-long in WTI and Brent crude oil by 61,000 lots to 1.06 million lots in the week to March 20. The overwhelmingly bullish sentiment can also be seen through the long/short ratio which last week stood at 12.5 to 1, the second highest on record.

2024: The wasted year

Markets are driven by election optimism, overshadowing growing debt and liquidity concerns. The 2024 elections loom large, but economic fundamentals and debt issues warrant cautious investment.

As US economic slowdown hints at a shift away from exceptionalism, USD faces downside with looming Fed cuts. AUD and NZD set to outperform as their rate cuts lag. JPY gains on carry unwind bets and BOJ pivot.

Amid AI and obesity drug excitement, equities see varied prospects: neutral on overvalued US stocks, negative on Japan due to JPY risks, positive on Europe. European defence stocks gain appeal.

With the economic slowdown, quality assets will gain favour, especially sovereign bonds up to 5 years. Central banks' potential rate cuts in Q2 suggest extending duration, despite policy and inflation concerns.

Commodities poised for rebound. The "Year of the Metal" boosts gold and silver, copper awaits rate cuts. Grains may recover, natural gas stabilises. Gold targets $2,300-$2,500/oz, copper's breakout could signal growth.

Markets are driven by election optimism, overshadowing growing debt and liquidity concerns. The 2024 elections loom large, but economic fundamentals and debt issues warrant cautious investment.

As US economic slowdown hints at a shift away from exceptionalism, USD faces downside with looming Fed cuts. AUD and NZD set to outperform as their rate cuts lag. JPY gains on carry unwind bets and BOJ pivot.

Amid AI and obesity drug excitement, equities see varied prospects: neutral on overvalued US stocks, negative on Japan due to JPY risks, positive on Europe. European defence stocks gain appeal.

With the economic slowdown, quality assets will gain favour, especially sovereign bonds up to 5 years. Central banks' potential rate cuts in Q2 suggest extending duration, despite policy and inflation concerns.

Commodities poised for rebound. The "Year of the Metal" boosts gold and silver, copper awaits rate cuts. Grains may recover, natural gas stabilises. Gold targets $2,300-$2,500/oz, copper's breakout could signal growth.