Lion Global Dynamic Growth SGD Q1 2021 commentary

| Asset classes | Stocks (developed and emerging markets), bonds (investment grade and high yield) and commodities |

| Instruments traded | ETFs and mutual funds |

| Investment style | Bottom up research and selection of best in class ETFs and mutual funds |

| Quarterly return | 1.04% (net of fees) |

| Annualised volatility (since inception) | 8.96% |

Market overview

Equity

Global markets were up 4.2%, lifted by a rapid vaccine rollout in the U.S. and U.K; increased evidence of vaccine efficacy; and sustained policy support in most major economies. The Biden administration’s aggressive stimulus spending further boosted markets in anticipation of an accelerated economic recovery in the U.S. as well as beneficial spillover effects with trading partners. Commodity prices continued their rise in March 2021, albeit at a more subdued pace. Emerging markets trailed developed due in part to the uneven distribution of vaccines in these countries, the stronger dollar, rising raw-materials costs, unrelenting supply-chain constraints, and elevated commodity and food prices.

U.S. equities gained 3.7% as investors weighed optimism about reopening against inflation and interest rate concerns. Biden’s ambitious agenda to overhaul the economy and to vaccinate 200 million Americans in the first 100 days of his administration boosted markets. U.S. yields continued to climb, and while signaling positive growth, introduced uncertainty as to whether the Fed will be able to effectively navigate an inflation spike.

European equity markets were up 6.1%. The European Central Bank (ECB) announced its intention to speed up bond purchases to counter a recent increase in bond yields, which the ECB President said reflect higher growth expectations in the U.S. rather than a recovery in Europe. While euro zone factory activity grew at the fastest pace in at least two decades, concerns lingered as lockdowns were reinstated in some countries and the slow pace of the EU vaccination campaign continued. U.K. equities rose a more tepid 4.1% on the government’s announcement to raise taxes starting in 2023 to cover the heavy costs of the pandemic.

Asia-Pacific markets gained 4.0%. Japanese equities, up 1.3%, seemingly shrugged off concerns about deflation, even as consumer prices fell further. Australian equities gained 2.4% as housing prices hit record highs, buoyed by ultralow interest rates, a big jump in household savings, and the Reserve Bank of Australia’s insistence that interest rates are unlikely to rise before 2024. Emerging markets (EM) fell 1.0%. The risk-on rotation into emerging markets may have been short-lived as investors became increasingly concerned over the uneven vaccine rollout and rising inflation.

Central banks, most notably within Turkey, Brazil, and Russia, hiked rates in an effort to curb inflation due in part to rising food prices. Chinese equities fell 6.0%, dragging down the broader EM index. China signaled plans to unwind its pandemic stimulus to cool an overheating economy and narrow a widening fiscal deficit. Both manufacturing and services Purchasing Managers’ Index (PMI) expanded in March 2021, fueled by strong overseas demand.

Fixed Income

US Treasury yields continued to climb in March 2021 on the back of improving US economic data expectations and risk sentiments. The steepening of the yield curves, while indicative of rising optimism about the global growth outlook, also indicated building inflationary pressures.

In March 2021, Asia credit performed in-line with other global indices. The JPM Asia Credit Index composite fell, returning -0.39%. Both Investment Grade (IG) and High Yield (HY) bonds posted declines in returns at -1.67% and -0.48% respectively. Spread-wise, HY spreads tightened by 10 basis points (bps) to 579bps while IG spreads tightened by 9bps to 183bps. The composite tightened by 8bps to 265bps. The tightening in spreads was unable to entirely offset the drop in US Treasury returns.

Portfolio performance (net of fees)*

| Jan | 0.85% |

| Feb | 2.19% |

| Mar | -1.96% |

| Since Jan 2016 | 75.0% |

Investment performance of the managed portfolio reflected for the period prior to the launch on 25/02/21 is simulated past performance, based on back-tested performance of portfolio components. For more detailed information, see full disclosure in the disclaimer section of the commentary.

Developed Markets equities have delivered positive absolute returns in the month of March 2021 which have seen Developed Markets equities component fund such as LionGlobal Japan Growth fund, Schroder ISF European Special Situations fund and BGF US Growth fund being key contributors to the Portfolio.

Emerging Markets equities have delivered negative absolute returns mainly driven by China equities underperformance. As such, component funds with large China equities exposures such as Schroder ISF Greater China fund and Goldman Sachs Asia Equity Portfolio Base fund become key detractors to the Portfolio.

On the fixed income side, rising US bond yields have resulted in underperformance of the fixed income component funds like the PIMCO Global Bond fund, Fidelity APAC Strategic Income Bond fund and BGF USD High Yield Bond fund. Gold prices have also fallen resulting in Aberdeen Standard Gold ETC being a detractor to the Portfolio.

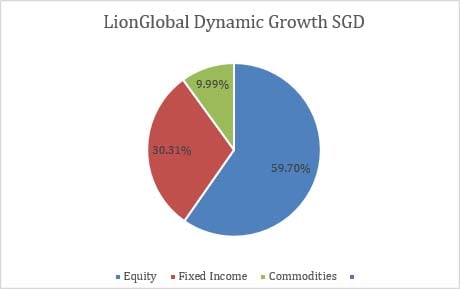

Portfolio Allocation (as of 31/03/21)

Outlook

Global growth momentum is expected to pick up pace from 2Q 2021 onwards. Strong business spending and goods demand have helped to sustain the boom in global manufacturing, pushing factory output above its pre-crisis path. Demand from services sector will now improve in the coming quarters and lead the next stage of the global recovery with vaccines rollout and easing of restrictions on mobility.

The US will be the main engine driving global growth this year, while Europe will be a laggard. In the US, the passage of the $1.9 trillion fiscal stimulus will further bolster the excess saving stock of US households and help the GDP to rise above its pre-COVID-19 path from 3Q 2021.

In China, while external demand should provide a material boost to industry, domestic demand will moderate. China’s National People’s Congress in March 2021 set new goals in the 14th Five-year Plan (2021-2025) for the long-range objectives through the Year 2035. China aims to double its income per capita by 2035 and set a 6% growth target for 2021. In the near term, both monetary and fiscal policies are expected to keep the economic recovery from 2020 pandemic on a steady footing. No sharp reversal of easy policies were announced or to be expected for 2021. China’s manufacturing and export recovery would also continue to support the trade and exports numbers of Korea, Taiwan and Singapore.

The key risks for the markets include (1) A sharper rise in inflation, accompanied by lower unemployment rates leading to an earlier-than-expected Fed tightening, (2) New strains/mutations of COVID-19 virus rendering current available vaccines ineffective and delaying the economic recovery, (3) A further escalation in US/China tensions, and, (4) Further rise of Chinese domestic defaults and potential contagion.

On Equities, a stronger world economy, with potential for additional US fiscal stimulus from infrastructure spending and the abundant liquidity provided by the central banks will keep the markets supported. The valuation of equities (Price-to-Earnings and the Price-to-Book) remain expensive vs historical averages, but fair when compared to bonds. While multiple expansions were the main driver of returns in 2020, earnings growth will be the key during this phase of the business cycle. As such, companies with strong earnings momentum and operating leverage are likely to be the beneficiaries with the opening up of the economies.

On Fixed Income, the bear steepening in the US Treasury curve reflects funding concerns for the US stimulus spending, as well as a return of inflationary risks. However, the front end interest rates remain very well anchored - by the Federal Reserve’s promise not to taper its asset purchases or hike interest rates anytime soon. The outlook is relatively constructive for Asian credit markets, though scope for further compression is marginal, especially for investment grade bonds. In comparison, high yield bonds have scope for credit spread tightening and are likely to benefit from investors’ hunt for yield. Central banks are expected to continue with supportive monetary and fiscal policies, amidst a trajectory of growth and improving corporate fundamentals from a low base.