- Currencies are a sea of calm, given the vicious gyrations on global bourses

- Asia is now leading the charge lower in deleveraging

- Today's close critical for establishing if sentiment revives or we face an all-out crash

View of the hammer to ring the closing bell of New York Stock Exchange on the NYSE balcony.

Pic: Shutterstock

Global equity markets continue to take the lead in driving the market action, with Asia and particularly China having a bad time of it. The key Chinese stock index is down almost 10% in the space of a week and down more than 5% overnight before bouncing late in the session. Both the Chinese and Japanese key indices are eyeing whether the 200-day moving average (Nikkei 21,000) will support, a moving average that also looks critical for the US S&P 500 (at 2538 for the cash index today). On that note and given market corrections and crashes of the past, it would seem that today’s close in New York is critical for establishing whether this market can find support for now or faces a more ominous downdraft.

A bit of market history: It was a Friday-Monday one-two that saw the majority of the 1987 panic in the US market, let us recall, that provided the majority of the bear market of the time – and it came after an 11% slide that in turn was in the wake of a parabolic ramp up in prices all summer as bond yields were spiking higher. The parallels are alarming, and investors should respect the risks once markets are inside the fat tail.

One likely source of considerable unease this week were the two US Treasury auctions on Wednesday and Thursday of 10-year and 30-year US Treasuries, respectively. These auctions saw sharply lower demand after very strong prior auctions in January. Combine this with a Fed that seems to be much more nonchalant about the magnitude of recent market volatility relative to past Fed officials, and the market may feel that the strike price of the Fed put may prove considerably lower in the Powell era. But most unsettling for so much money under management in the world is that “risk parity” is not working at all at the moment as long yields have remained high (bonds very weak) even as we have outright carnage in equity markets. With the hundreds of billions and even trillions of dollars in management under these assumptions, the pain trade is more of the same with nowhere for these money managers to hide.

In FX, meanwhile, there are signs of nerves, but not much else: some of the commodity currencies are weak, but in the case of CAD and RUB, this is easily attributable to the chunky selloff in crude oil in recent sessions. EM currencies are mostly offered, but not in any way that suggests much contagion pass-through, though we are starting to see some of the classic risk signals for EM, including EM sovereign yield spreads starting to widen out noticeably yesterday.

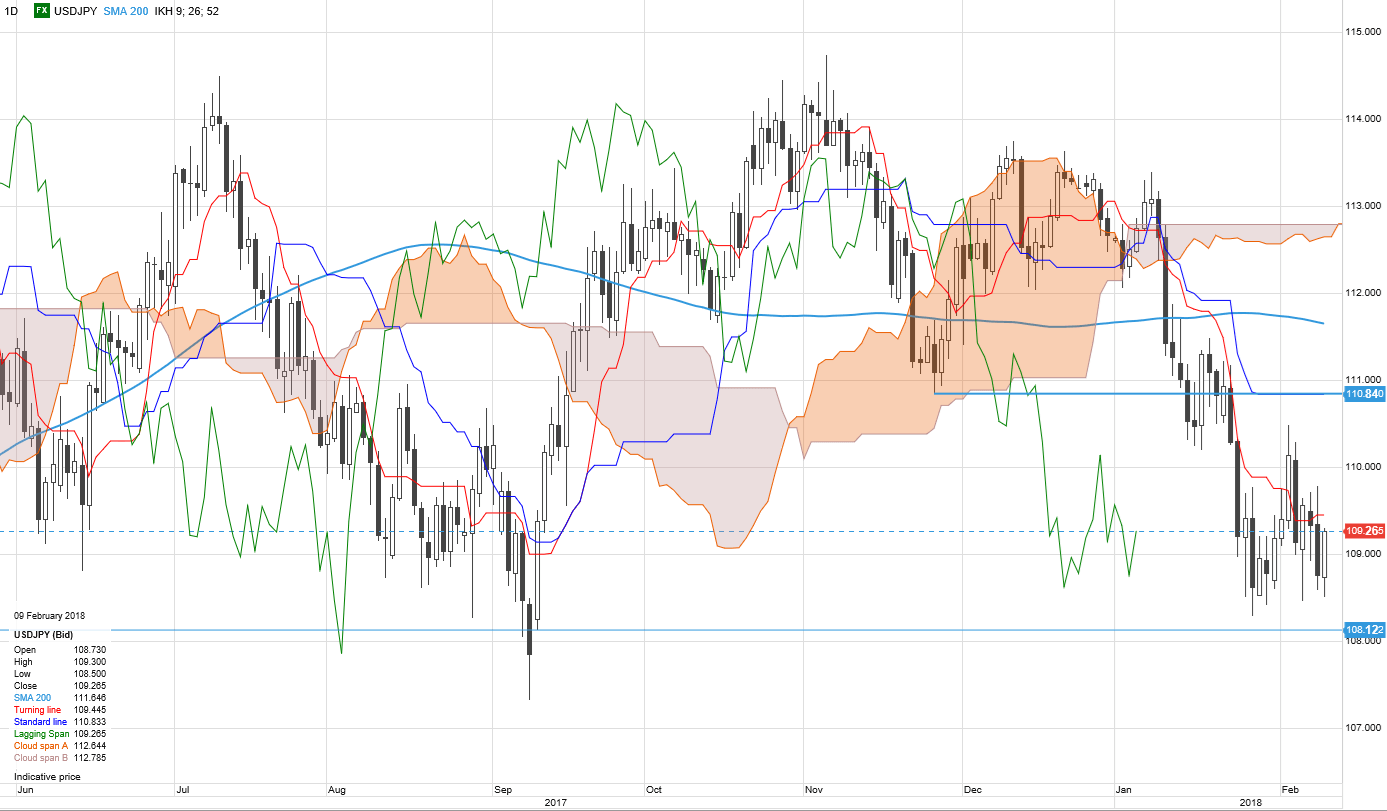

Within G10, JPY crosses are very quiet – USDJPY still stuck near 109.00 despite yesterday’s ugly session and further tremors in Asia. CHF has been a bit more on the move as EURCHF has melted through local 1.1500 support yesterday but has bobbed back above that level on the pause in the equity deleveraging this morning in Europe.

The Russian central bank meets later today and has an interesting backdrop for their decision. After the recent record low Russian CPI inflation print and huge drop in the oil price, it would have seemed a no-brainer to cut the policy rate 50 basis points rather than the 25 basis points the consensus supposedly expects, but recent market volatility raises the odds of a 25 bps move.

Chart: USDJPY

The resilience in FX is remarkable. While it is clear from the options market that interest in downside hedge protection in JPY crosses has picked up strongly, currencies remain a sea of calm relative to the scary backdrop. We continue to eye the 108-107.50 zone as technically important here, and likely also important because Japanese exporters who have been complacently assuming that the Bank of Japan's Kuroda would always have their back and keep the JPY weak may feel forced to hedge in droves if key supports are broken here.

Source: Saxo Bank

The G-10 rundown

USD – there seems to be little for the US dollar here from the latest risk wobbles, though it has tended stronger versus the most risk-correlate currencies. The market will be happy to sell the USD if markets calm again and a recovery in EURUSD back above 1.2300-25 could market a technical turnaround for that key pair.

EUR – the euro selling has been modest, suggesting that any deleveraging (squaring of euro longs) linked to equity market gyrations has been likewise modest. Still, we note potential risk in EURJPY downside linked to relative speculative positioning in the two currencies if this risk contagion starts to hit across markets.

JPY – the yen strength from last yesterday has eased notably as early European hours have seen a bit of a bounce in animal spirits. As we note above, today’s close looks key.

GBP - pointedly hawkish Bank of England yesterday says it needs to hike more and faster than it thought was necessary in November. Sterling rallied hard in response, but the rally was largely disrupted by all of the risk-on, risk-off behavior yesterday, so we may need calmer markets for sterling to regain its rally legs.

CHF – EURCHF dipped well below 1.1500 during the most heated moments of weak risk appetite yesterday but has recovered back above this morning. For the short term, this safe haven behavior for the franc will likely dominate.

AUD – AUDUSD weakened precisely to the 200-day moving average just above 0.7750 and there is a 61.8% Fibo just below, so support needs to be found here or the downside pivot has been triggered.

CAD – weak on weak oil prices. Watching the 1.2600-65 zone intently in USDCAD over Canada’s jobs data later today – after two absurdly strong payrolls readings over the prior two months, the risk of a stronger mean reversion than the expected +10k for January is a distinct risk.

NZD – the weakness from the Reserve Bank of New Zealand statement has abated quickly and NZD seems to be oddly immune to the market backdrop.

SEK – EURSEK highs above 10.00 are suddenly in sight as SEK tends to perform poorly when risk appetite is wobbly.

NOK – NOK was floored by a very weak CPI this morning and with energy prices heavily offered we suddenly face the risk of a full test of the cycle highs near 10.00 if 9.8150 can’t provide resistance, especially if risk appetite can’t find a floor here.

Upcoming Economic Calendar Highlights (all times GMT)

- 0930 – UK Dec. Manufacturing Production

- 0930 – UK Dec. Visible Trade Balance

- 1030 – Russia Central Bank Rate Announcement

- 1330 – Canada Jan. Net Change in Employment / Unemployment Rate

- 1645 – UK BoE’s Cunliffe to Speak